PAGE 33

In spite of the many advantages of providing workforce benefits, some employers may

choose to drop health insurance coverage fully or partially. Employers may also benefit from

restructuring the work force to minimize the impact of the pay-or-play penalty (i.e. number

of hours employees work). Employers offering limited benefit plans may consider dropping

coverage as an alternative.

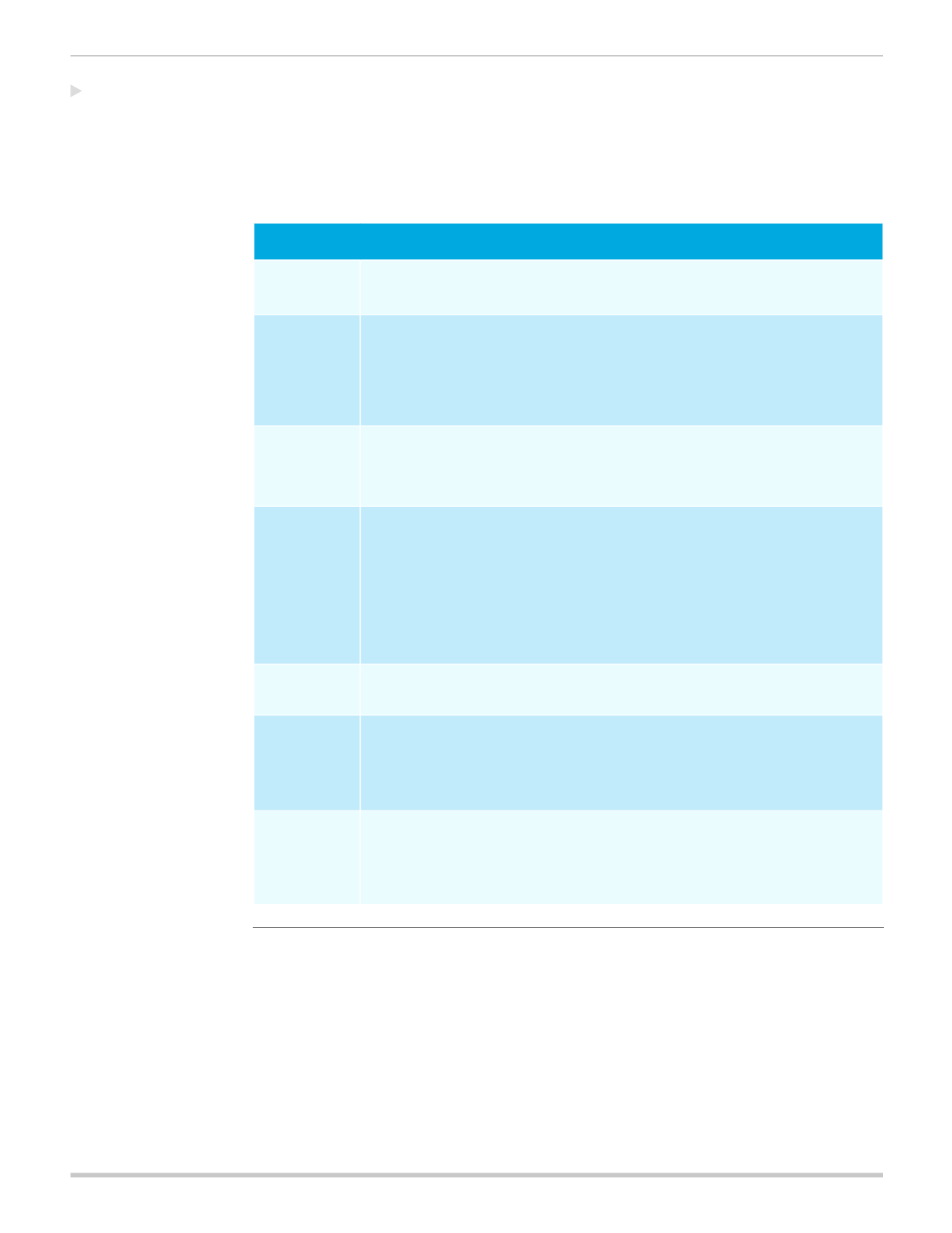

Discontinuing Coverage

Coverage

• Employees can obtain coverage in the Individual Market – both private marketplaces

and the public Health Insurance Marketplace.

Compliance

• Employer will no longer need to comply with requirements that are applicable

to employer providing health plans.

• Employers must notify employees regarding the availability of the Health Insurance

Marketplace and subsidies that could help lower the cost of insurance coverage (by

October 1, 2013, and for all new employees at the time of employment).

Tax Credits

• Employers will not be eligible to receive tax credits.

• Employees may be eligible to receive subsidies based on household income level and

other eligibility requirements through the Health Insurance Marketplace.

Penalties

• Starting in 2015, employers with 100 or more full-time equivalent employees may

be subject to shared responsibility penalties if coverage either does not meet

affordability or minimum value requirements, and is offered to fewer than 70 percent

of its full-time employees and the dependents of those employees (unless the

employer qualifies for 2015 dependent coverage transition relief).

• In 2016, the 70 percent threshold is increased to 95 percent and the shared

responsibility penalties will also apply to employers with 50 or more full-time

equivalent employees.

Administration • Employers will need to provide appropriate communication, education and support to

help employees obtain coverage in the individual market.

Employee

Tools and

Resources

• Employees will need to use the Health Insurance Marketplace during open enrollment

and special enrollment periods to obtain coverage if they are eligible for subsidies.

• Employees may also use the private marketplaces for enrollment during designated

open enrollment or special enrollment periods.

Supplemental

Insurance

Protection

• The employer can continue to provide voluntary benefits regardless of discontinuing

major medical coverage.

• These policies can be bought separately to help employees cover out-of-pocket

costs associated with illness or injury.

Discontinuing

Coverage