PAGE 28

In the post-reform environment, private marketplaces (also known as exchanges) will become

a viable option with the guaranteed issue of coverage and an employer’s ability to provide a

defined benefit or defined contribution toward employee coverage. Employers of all sizes can

choose the private marketplace to provide employee benefits packages.

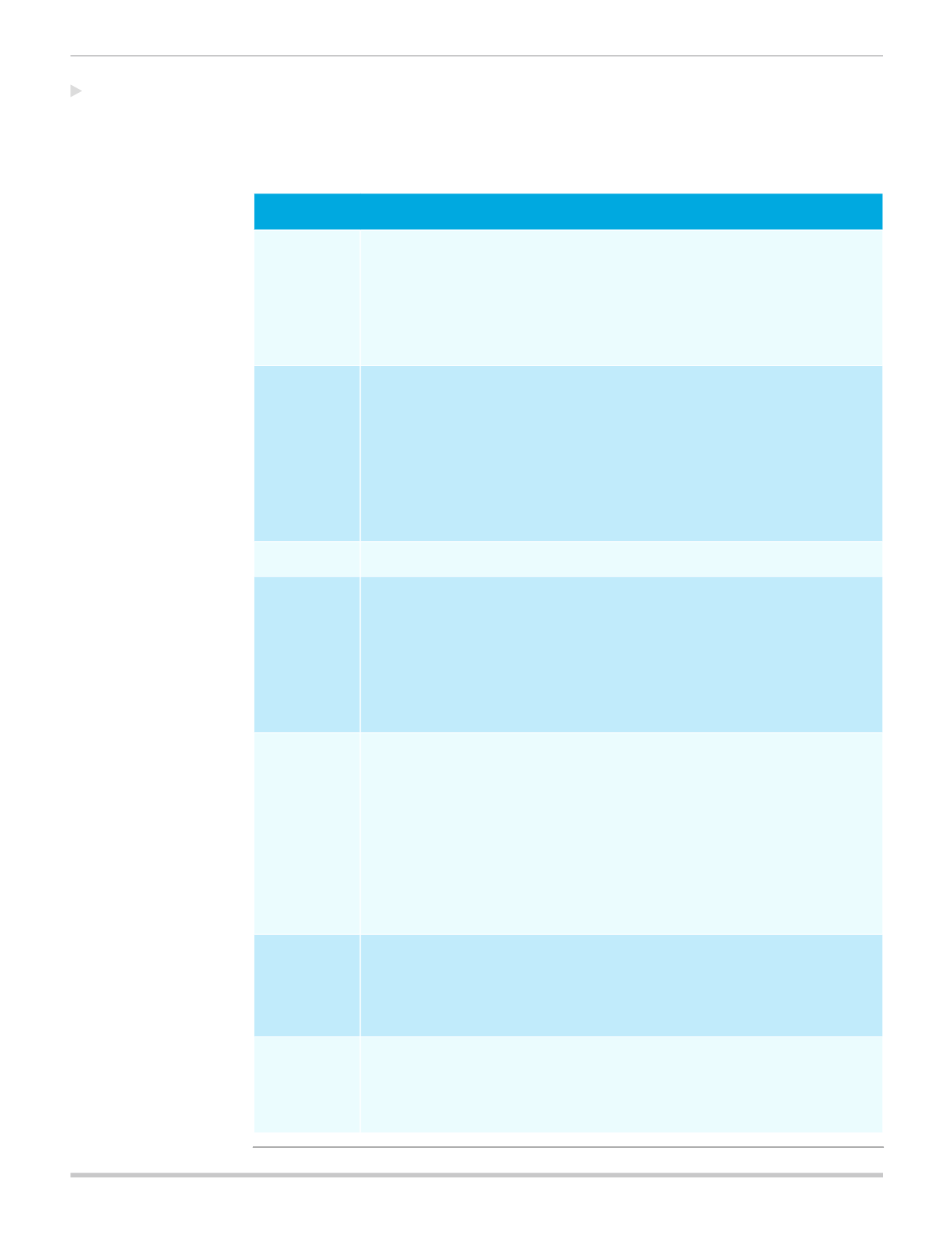

Private Marketplace

Coverage

• Employees will be able to obtain coverage regardless of health status beginning 2014.

• The employer can choose which coverage model they want to offer their workforce:

defined contribution (a specific dollar amount employees can choose towards a plan)

or defined benefits (specific plan(s) employees can choose from).

• Plans will vary based on model choice, and specific details provided by the

marketplace.

Compliance

• An employer will need to comply with all applicable federal and state laws and rules.

• The employer will need to comply with the new Affordable Care Act (ACA) benefit

mandates including metal levels and/or minimum value requirements.

• The employer needs to be aware of all the ACA compliance requirements, specifically

the benefit mandates, and grandfathering, that directly affect them.

• Employers must notify employees regarding the availability of the Health Insurance

Marketplace and subsidies that could help lower the cost of insurance coverage (by

October 1, 2013, and for all new employees at the time of employment).

Tax Credits

• Employers will not be eligible to receive tax credits.

Penalties

• Starting in 2015, employers with 100 or more full-time equivalent employees may

be subject to shared responsibility penalties if coverage either does not meet

affordability or minimum value requirements, and is offered to fewer than 70 percent

of its full-time employees and the dependents of those employees (unless the

employer qualifies for 2015 dependent coverage transition relief).

• In 2016, the 70 percent threshold is increased to 95 percent and the shared

responsibility penalties will also apply to employers with 50 or more full-time

equivalent employees.

Administration • Employers will need to submit employee information to the private marketplace.

• Depending on the marketplace, it may issue employers a single invoice and collect

payments.

• Employers will need to perform employee payroll deductions to pay premiums.

• Employers will work with the marketplace to reconcile enrollment information, billing

and termination functions.

• Private marketplaces may assist in meeting the compliance reporting requirements

that are in place for employers starting in 2016.

Employee

Tools and

Resources

• Employees use the private marketplace during open enrollment.

• Employees will submit an application for enrollment and select the plan.

• Employees may be required to use the private marketplace for all updates, special

enrollments, terminations and other applicable functions.

Supplemental

Insurance

Protection

• Private marketplaces may have a full benefits package including voluntary coverage,

but it will vary depending on the marketplace.

• These policies can be bought separately to help employees to cover out-of-pocket

costs associated with illness or injury.

Private

Marketplace