PAGE 29

An employer-sponsored health plan can be grandfathered if it covered employees when

the ACA was enacted (March 23, 2010), and if the plan does not make certain material

changes that lower benefits or employer contributions, or increase employee paid deductible,

coinsurance or copayment costs to the employee. While grandfathered plans may have lower

rates (at least in the initial years), they are not required to include some of the new ACA benefit

reforms.

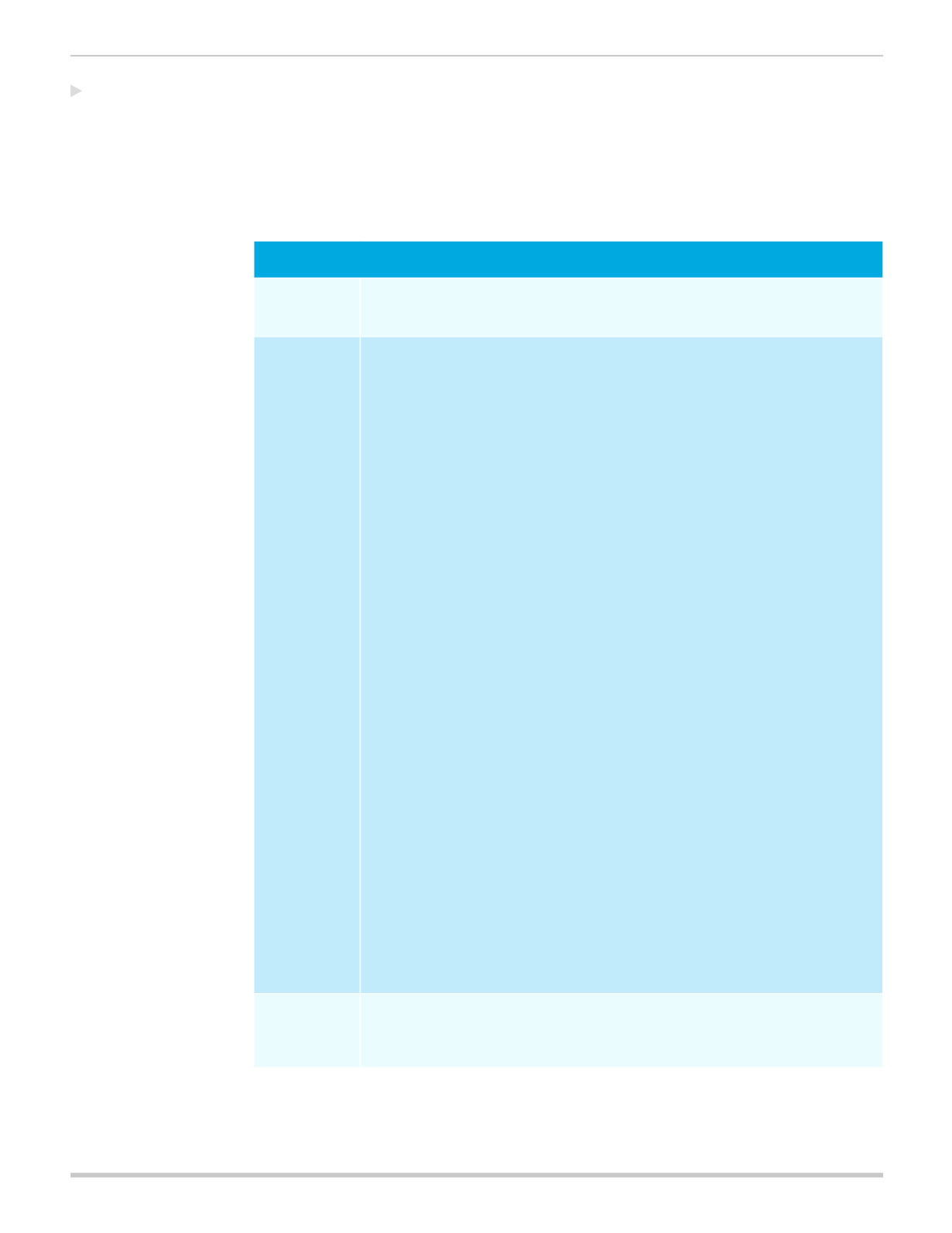

Maintain Grandfathered Status

Coverage

• Employers will continue to offer the pre-reform grandfathered benefit plans.

• The benefit plan cannot change in certain ways (see list below).

Compliance

• The employer will need to comply with all applicable federal and state laws and rules,

including some of the new ACA provisions, including the prohibition on annual and

lifetime limits on essential health benefits, the prohibition on pre-existing condition

exclusions, requirements for coverage of adult children to age 26, and the 90-day

limitation on waiting periods.

• Employees need to be notified of the grandfathering status.

• The employer must notify employees regarding the availability of the Health Insurance

Marketplace and subsidies that could help lower the cost of insurance coverage (by

October 1, 2013, and for all new employees at the time of employment).

• Grandfathered plans are exempt from certain health care reform provisions, such as:

-- Certain benefit mandates, such as essential health benefits or requirements to

cover preventive benefits with no cost-sharing

-- Clinical trial coverage

-- External appeals process

-- Non-discrimination testing for fully insured plans

-- Maximum out-of-pocket and deductible limits

-- Some of the additional reporting and disclosures

-- Guaranteed availability and renewability

• Grandfathered plans may change insurance companies, as long as there is no

change in coverage as described below.

• Grandfathered plans cannot:

-- Significantly cut or reduce benefits

-- Raise employee co-insurance charges

-- Significantly raise co-payment charges (15% more than medical trend since 2010)

-- Significantly raise deductibles (15% more than medical trend since 2010)

-- Significantly lower employer contributions (more than 5% of proportional cost share

for any coverage category)

-- Add or tighten an annual limit on what the plan pays

-- Starting in 2014, no annual dollar limits

Tax Credits

• Employers will not be eligible to receive tax credits.

• Employees may be eligible to receive tax credits through the Individual Exchange

if their employer’s coverage does not provide affordable, minimum value coverage.

Maintain

Grandfathered

Status

continued on next page